TL;DR

Adding Paua Solo to a salary sacrifice portfolio lets providers offer tax-efficient public charging to all employees, including those without home chargers. Integration is simple via manual upload or API, delivering one card, one dashboard, and one invoice. The result is higher take-up, simplified admin, compliance confidence, and expanded market reach.

Adding Paua Solo to Your Salary Sacrifice Portfolio: The Integration Guide

How to plug in the UK’s leading tax-efficient public charging solution

Salary sacrifice EV schemes are booming; and for good reason. They make driving electric accessible, affordable, and attractive. But as the market matures, one critical question is emerging from employers and drivers alike:

“How do we handle public charging?”

That question has created both a challenge and an opportunity for salary sacrifice providers.

The challenge: most schemes were built around vehicles and (perhaps) adding a home charger.

The opportunity: by adding Paua Solo (the EV charge card for salary sacrifice), providers can now deliver tax-efficient public charging too, completing the package and expanding their eligible market by up to 44%

Here’s how to make that happen; step by step.

1. Why integrate Paua Solo?

Let’s start with the “why.” Adding Paua Solo strengthens your product portfolio across four dimensions:

1. Inclusivity

Home charging works for only 56% of employees. Paua Solo makes your scheme work for everyone, including renters, apartment dwellers and city-based drivers.

2. Compliance

Paua Solo uses a gross pay (pre-tax) model, so every deduction is HMRC-aligned and clearly documented. No post-pay grey areas.

3. Simplicity

Employers love it because it’s “one card, one invoice, integrated with the car.” Scheme providers love it because it’s “one data feed, one dashboard, no admin.”

4. Growth

Adding public charging to your offer can increase eligible driver volumes by up to 78%, according to modelling from Paua’s business case (just ask us – we will happily send the workings over!)

In other words: it’s a commercial, operational and ethical win all at once.

2. How Paua Solo works (in 60 seconds)

- The scheme provider includes Paua Solo as an optional add-on when the employee selects their EV.

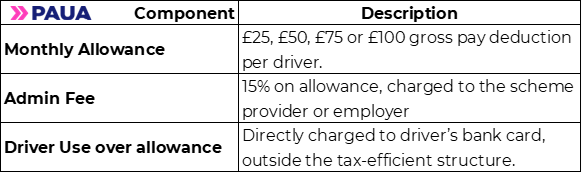

- The employee chooses a monthly public charging allowance; typically £25, £50, £75 or £100

- That amount is deducted from gross salary before tax and NI.

- Paua loads the allowance each month onto the driver’s Paua Solo EV charge card account.

- The card works at 65,000+ public connectors (October 2025) across 50+ networks nationwide

- Any unused balance rolls over; if the driver goes over, the difference is billed to their personal debit card.

Everything is tracked in the Paua dashboard and the driver can review their balance in the app; one place, one record, one set of numbers.

3. Integration models: choose your route

Scheme providers can integrate Paua Solo in one of two ways, depending on their platform maturity and technical capacity.

Option 1: Manual upload (fastest route to market)

Best for: providers with smaller fleets or early-stage digital systems.

How it works:

- You share a secure dataset of new drivers each month: name, email, employer, allowance, start date.

- Paua sets up their accounts, issues charge cards, and manages monthly top-ups.

- You receive one consolidated invoice for all drivers at month-end.

This route takes days, not months, to go live; and is ideal for pilot programmes or early-stage launches.

Option 2: API integration (seamless automation)

Best for: established providers with digital platforms or custom portals.

How it works:

- Paua’s open API connects directly to your salary sacrifice platform.

- Driver data (including allowance and employer details) syncs automatically when a new car order is placed.

- Invoices and usage reports flow back in real time for reconciliation.

Benefits:

- No manual handling.

- Near-zero admin.

- A “native” experience for your customers.

Paua provides full technical documentation, sandbox access, and an onboarding engineer to ensure integration runs smoothly.

4. Step-by-step integration process

Here’s how most providers bring Paua Solo to life; typically in under four weeks.

Step 1: Scoping call (Week 1)

Paua’s partnerships team runs a short onboarding workshop to understand your platform, customer base, and data flow. Together, you agree on:

- Launch timeline

- Integration model (manual, API, or white-label)

- Pricing and service fee structure

- Reporting format and frequency

Step 2: Setup (Week 2)

Paua provides your team with:

- Implementation pack (data templates, brand guidelines, pricing guide)

- Data requirements

Step 3: Pilot (Week 3)

You onboard a small number of employer customers to test the process end to end; from payroll deduction to charging in the real world.

Paua monitors card issuance, charging activity and reporting accuracy to ensure everything aligns.

Step 4: Full launch (Week 4)

Once validated, you roll out Paua Solo across your portfolio. Paua handles scaling, customer support, and network expansion in the background.

The result: you can advertise “Public Charging Included” across your salary sacrifice marketing with confidence and compliance. Add the Paua Solo EV Charge Card for salary sacrifice schemes with the maximum reach to drivers.

5. Commercial structure

Paua Solo has a simple, transparent model designed to fit within salary sacrifice pricing frameworks.

No hidden costs. No per-session fees. No reconciliation drama.

This clarity makes Paua Solo easy to model into existing provider pricing.

6. Marketing and sales enablement

Once live, Paua supports partners with a full marketing toolkit, including:

- Co-branded brochures and one-pagers.

- Web and email copy templates.

- Imagery, icons, and key data visuals.

- Case studies and ROI examples (e.g., 78% volume uplift, 42% average driver savings).

Scheme providers can quickly position themselves as the inclusive, tax-efficient EV benefit solution; a big differentiator against legacy players or emergent challenger brands.

7. Compliance confidence

As covered in an earlier blog, Paua’s gross pay model ensures each deduction is pre-agreed and clearly contractually defined. That means:

- Salary sacrifice integrity is preserved.

- HMRC reporting remains straightforward.

- Employers can show transparent, auditable deductions.

Paua also supports providers with template contract wording and payroll guidance to help employers implement the solution correctly.

8. What integration success looks like

When Paua Solo is integrated well, scheme providers typically see:

- Faster employer onboarding (no compliance objections).

- Higher take-up among renters and flat dwellers.

- Simplified monthly reconciliation across payrolls.

- Reduced inbound support tickets.

- Stronger ESG alignment in marketing and tenders.

Most importantly, they gain a genuinely differentiated offer; one that treats charging as a core benefit, not an afterthought.

9. Looking ahead: Paua Solo as standard

As more employers expect salary sacrifice schemes to include public charging, integration is shifting from optional to essential.

By embedding Paua Solo now, providers position themselves for the next phase of the market; where inclusivity, simplicity and compliance are the default expectations, not extras.

10. Conclusion: one integration, endless impact

Adding Paua Solo to your salary sacrifice portfolio is more than a product upgrade. It’s a way to make EV benefits work for everyone; fairly, simply, and profitably.

Whether you start with a quick manual upload or go fully automated through API, Paua’s team will help you design a setup that fits your business, your clients, and your drivers.

One card. One platform. One step closer to an inclusive electric future.

Get started today; and turn public charging from a gap in your portfolio into a growth engine for your business.

Paua Solo is the EV charge card solution for public charging in your salary sacrifice scheme. Contact Paua to learn how EV drivers can save up to 62% on public EV charging through salary sacrifice. Get cheaper, tax-efficient EV charging with Paua.

*This content is for general information only and does not constitute tax advice.

Paua is a business EV charging payment platform that enables fleets to manage public, home and workplace charging in one system.

Read more about Paua Salary Sacrifice here.

.jpg)