TL;DR

EV salary sacrifice schemes can fund public charging in two ways: gross pay (pre-tax) or post-pay (after use). Paua Solo’s gross pay model ensures HMRC compliance, predictable savings of up to 62%, and minimal employer risk. In contrast, post-pay models create tax uncertainty, variable costs, and potential payroll complications.

Gross Pay vs Post-Pay: The Two Ways to Fund Public EV Charging - and Why One Is Safer

The hidden tax question at the heart of EV salary sacrifice

As salary sacrifice EV schemes evolve, more drivers are discovering the benefits of adding public charging to their package. But there’s a subtle, and vital, question that determines how safe, simple, and compliant that benefit really is:

Do you fund the charging before tax or after?

That single decision separates two models: gross pay (pre-tax) and post-pay (after use). And while they might sound similar on the surface, they operate very differently in the eyes of payroll, HMRC, and the employer’s risk register.

Let’s unpack how each works, what the tax implications are, and why the gross pay model used by Paua Solo offers scheme providers and employers the confidence they need.

1. Understanding the two models

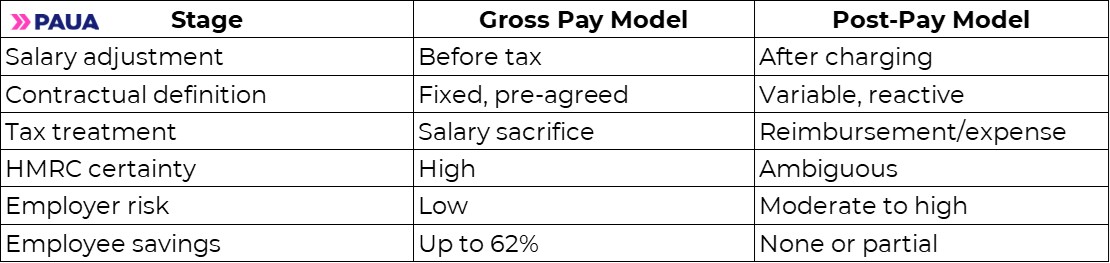

A. The Gross Pay Model (Pre-Tax Deduction)

In this model, the employee agrees to sacrifice a fixed amount of gross salary each month, before tax and National Insurance. That amount funds a charging allowance on their Paua Solo card.

Think of it as pre-loading an account with a fixed value. The driver then uses that balance for public charging at any of Paua’s 65,000+ UK connectors across 50+ networks

The deduction is simple:

- Payroll adjusts gross salary by the agreed amount (e.g. £50/month).

- The employee’s taxable income is reduced accordingly.

- HMRC sees a clean, auditable salary sacrifice arrangement.

If the driver uses less, the balance rolls over; if they use more, the excess is paid personally via their own debit card. Everything is visible and predictable.

The result: clear compliance and defined tax savings.

B. The Post-Pay Model (After-Use Deduction)

This is where others operate differently.

Instead of pre-allocating a gross salary amount, drivers simply charge their vehicles as normal, either at home, at work, or in public. Then, at the end of each month, the cost of that usage is deducted after the fact from their salary.

In theory, this feels “flexible”: you only pay for what you use. But in practice, it means the salary adjustment is being made after the service has been consumed - creating uncertainty around whether it truly qualifies as a salary sacrifice deduction under HMRC rules.

The issue isn’t the intent; it’s the timing.

Generally salary sacrifice must be contractually agreed in advance, not calculated based on variable, retrospective usage. That’s where post-pay models walk a tightrope.

2. The compliance question

HMRC guidance is clear: salary sacrifice must be a contractual variation agreed in advance, setting out the amount of salary to be given up and the benefit received in return.

In a gross pay model like Paua’s, this is black and white.

- The agreement states: “Employee sacrifices £X of gross salary monthly for an EV charging allowance worth £X.”

- The amount is fixed and documented.

- Tax and National Insurance are adjusted accordingly each month.

In a post-pay model, the deduction is reactive.

- The amount isn’t known until after the charging occurs.

- The deduction may vary month to month.

- HMRC could consider this a reimbursement or expense adjustment, not a salary sacrifice - which means no tax or NI relief.

Worse, if challenged, the employer (and scheme provider) could be exposed to backdated liability for unpaid tax or NI.

It’s not that these schemes are illegal - but they are interpretive, and interpretation is not a compliance strategy.

3. The risk sits with the employer and provider

Under salary sacrifice legislation, the employer is responsible for ensuring that the structure is compliant. Scheme providers, in turn, are responsible for ensuring what they deliver aligns with that structure.

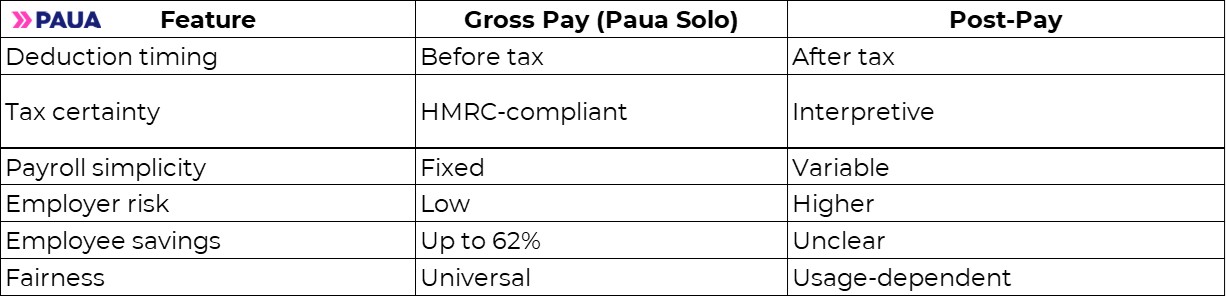

That’s why Paua designed Solo from the ground up as a gross-pay-first system. Every deduction happens before the benefit is delivered.

With post-pay systems:

- Employers face potential payroll corrections.

- Scheme providers risk mis-categorising benefits.

- Auditors may question whether PAYE reporting was correct.

- Drivers lose confidence when the numbers change each month.

Gross pay avoids all of that.

4. Predictability: good for drivers, better for payroll

Drivers don’t want complexity. They want a fixed monthly package they can understand.

Under the Paua Solo model, a driver knows exactly what they’re getting - say, £50/month of charging deducted pre-tax. Their savings are consistent (typically around 42%, depending on tax band) and their public charging becomes a predictable line on their payslip.

For payroll teams, that consistency is gold. One line. One fixed amount. One set of tax codes.

Compare that to post-pay: variable deductions, inconsistent values, and re-work in every pay cycle. And a minimum wage risk.

Simple maths wins.

5. Why timing defines the tax

The difference between the two models boils down to a single line in the payroll calendar:

It’s not just an operational preference - it’s a fundamental legal distinction.

6. Why Paua chose gross pay on purpose

Paua Solo was designed with scheme providers, employers, and auditors in mind. The aim was to give everyone confidence that the charging component of salary sacrifice is as cleanly structured as the car lease itself.

That means:

- Fixed top-ups of £25 / £50 / £75 / £100 per month

- One source of truth via Paua’s reporting dashboard

- Monthly invoices to scheme providers with transparent +15% admin fee

- Audit-ready data for payroll, HR, and compliance teams

Every transaction is clear: what was deducted, when, and what value was delivered to the driver.

7. The fairness factor

Fairness is an often-overlooked part of compliance. A gross pay model ensures every driver in a scheme is treated equally, regardless of how much they charge in public.

- Drivers who can’t charge at home aren’t penalised.

- Drivers who charge less simply roll their balance forward.

- Employers can offer the same tax-efficient package across the board.

Contrast that with a post-pay structure, where costs can vary wildly and the benefit becomes unpredictable or even inequitable.

A transparent, fixed structure not only satisfies HMRC but also supports ESG and inclusion goals by ensuring equal access to benefits.

8. The bigger picture: trust in the salary sacrifice market

Salary sacrifice is a powerful tool, but its reputation depends on trust. If schemes become associated with grey areas or retrospective deductions, that trust erodes quickly.

By adopting a gross-pay-first model, Paua ensures:

- Compliance confidence for providers and employers.

- Predictable savings for drivers.

- Clear communication for auditors and tax advisors.

In short: the cleanest path to tax efficiency without risk.

9. Summary: why gross pay wins

The bottom line

The best salary sacrifice schemes are built on three principles: fairness, simplicity, and compliance.

Paua Solo’s gross-pay approach delivers all three - giving scheme providers the ability to grow their portfolio, employers the assurance of compliance, and employees the confidence that their savings are real and risk-free.

When it comes to salary sacrifice EV charging, timing isn’t everything -

it’s the only thing.

Paua Solo isthe EV charge card solution for public charging in your salary sacrifice scheme. Contact Paua to learn how EV drivers can save up to 62% on public EV charging through salary sacrifice. Get cheaper, tax-efficient EV charging with Paua.

*This content is for general information only and does not constitute tax advice.

Paua is a business EV charging payment platform that enables fleets to manage public, home and workplace charging in one system.

Read more about Paua Salary Sacrifice here.

.jpg)